SpaceX listed on the Nasdaq on June 12, 2026, under the ticker SPCX, priced at $135 per share and a $1.77 trillion total valuation. That made it the seventh-largest company in the United States by market capitalisation and approximately the two-hundredth by revenue. By June 18 it had posted its first post-IPO decline. By June 19, a Bloomberg columnist was comparing it to a meme stock. Nothing changed about the company between June 11 and June 12. Nothing changed about the company between June 12 and June 18. What changed was the listing — and then what happened after the listing. Crypto markets ran this sequence for a decade before it arrived in traditional equities. The mechanics are identical. The vocabulary is new.

What the Valuation Gap Looks Like

Two independent valuations of SpaceX arrived within days of the IPO. Morningstar analyst Nicolas Owens built a discounted cash flow model and arrived at approximately $780 billion as fair value — less than half the $1.77 trillion listing price. His published conclusion: SpaceX is “overvalued in almost any scenario, at least in the near term.” His moonshot scenario — the most optimistic case, requiring SpaceX to achieve Starlink dominance, rapid Starship commercialisation, and sustained defence contract growth simultaneously — carried only a 7% probability and still reached only $1.3 trillion. Morningstar’s advice to investors: wait for insider selling post-lockup.

Aswath Damodaran, the NYU finance professor widely known as the “Dean of Valuation,” published his own analysis on Substack after the prospectus was released. His central estimate for SpaceX’s equity value was approximately $1.25 to $1.3 trillion — roughly 28% below the Nasdaq listing price. Damodaran is not a SpaceX sceptic. His model explicitly values Starlink as a dominant satellite internet business and Starship as a platform with genuine long-term commercial potential. His $1.3 trillion is his best-case reading of the company’s value, not a dismissal of its prospects. It is still 28% below what the IPO priced it at.

The underlying numbers support both analysts’ scepticism. SpaceX reported approximately $4.28 billion in net losses. Its free cash flow was approximately negative $9 billion. The price-to-sales ratio at the IPO price ranged from 60 to 141 times depending on the revenue period used. Robert Greifeld, the former chief executive of Nasdaq, went on CNBC and said SpaceX “represents a stock that’s trading not on fundamentals” but on “aspiration.”

These are not marginal critiques from short-sellers. They are the independent conclusions of Morningstar’s institutional research, the most cited independent valuation analyst in finance, and the former head of the exchange that listed the stock. The valuation gap between $780 billion and $1.77 trillion is not a matter of opinion about the company’s quality. It is a measurement of how far the listing price travelled from the range where independent analysts, using conventional financial methodology, can place the company’s value.

The Meme Stock Label Arrives

On June 19 — seven days after the IPO — a Bloomberg columnist published a piece warning that SpaceX, alongside Samsung and SK Hynix, was beginning to act like a meme stock. CryptoRank had already run the headline: “SpaceX is trading like a meme stock after its record IPO.” Both publications reached for the same vocabulary independently, within days of the listing’s first sustained price weakness.

The meme stock comparison is being used, in these pieces, primarily as a description: the price is disconnecting from fundamentals in the way meme stocks do. But it is worth asking where “meme stock” behaviour comes from — what produced it, who developed the mechanics, and why those mechanics are now appearing in the context of a Nasdaq listing for one of the most technically credible private companies in the world.

The answer is not Reddit. Reddit was the distribution channel. The underlying mechanics were developed in crypto markets, refined over thousands of individual events, and exported into equity markets once the retail infrastructure — commission-free trading, fractional shares, 24-hour mobile access to markets — closed the gap between how crypto and equities could be traded. The meme stock era of 2021 was not a spontaneous eruption of retail sentiment. It was the first time crypto market psychology arrived in equity markets with sufficient retail infrastructure to execute at scale.

What Crypto Invented

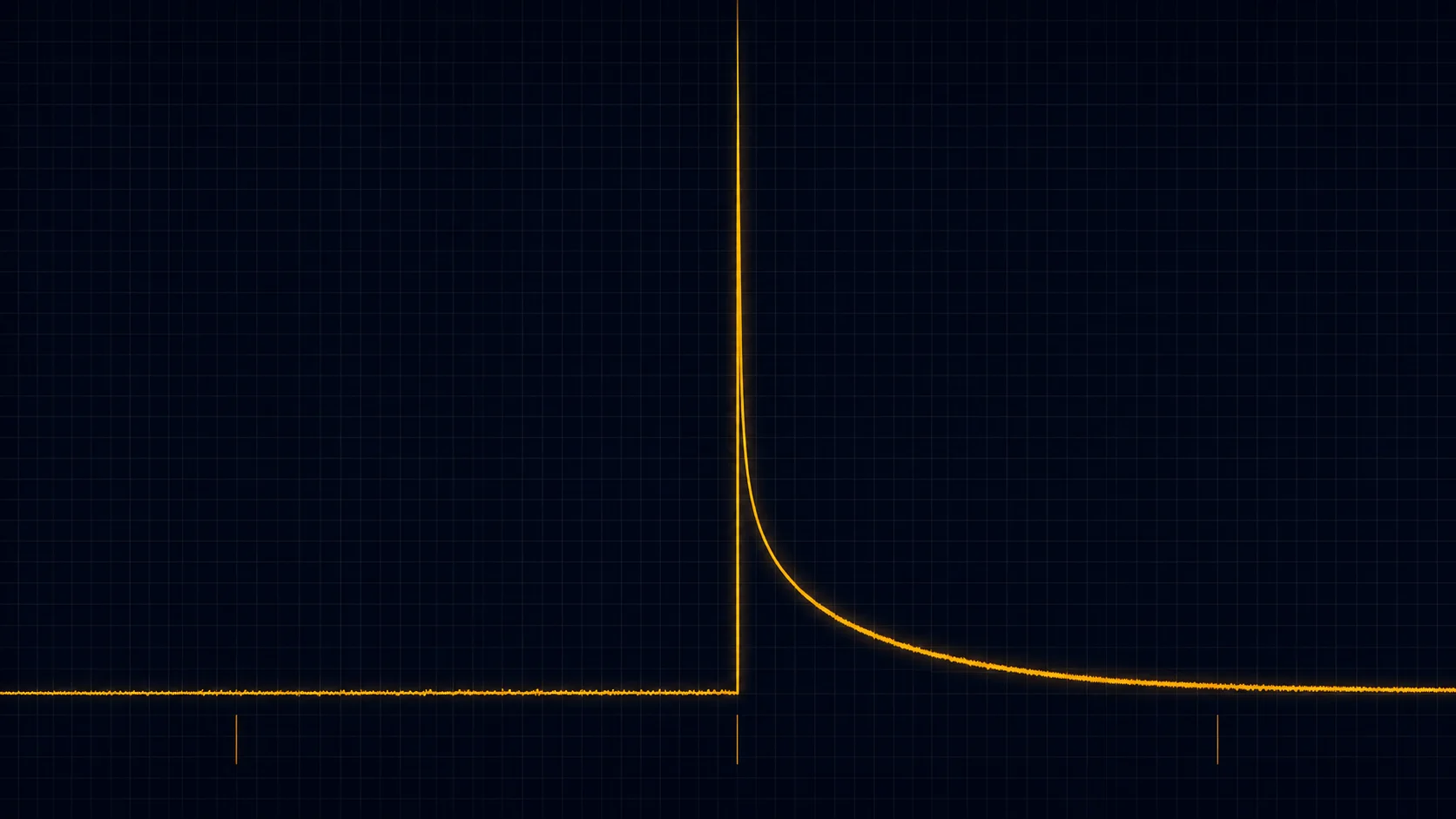

The academic documentation of crypto listing mechanics is precise. Xu and Livshits, in research published at the USENIX Security Symposium in 2019, monitored approximately 100 organised Telegram channels conducting coordinated pump-and-dump operations across the crypto markets of 2018. They recorded 412 individual pump events. Their core finding: organiser administrators pre-purchased the target coin before announcing it to channel participants, generating an information asymmetry that allowed insiders to sell into the retail buying wave they themselves created.

The timing data from their research is the most instructive part. In a documented case study of a single pump event — a coin identified only as BVB — the price reached its peak within 18 seconds of the pump announcement. Three and a half minutes after the pump began, the price had dropped back below its opening level. The entire cycle — maximum FOMO, peak price, insider exit, retail loss — completed in less time than it takes to read this paragraph.

The speed difference between an 18-second crypto pump and a multi-week IPO story is real but structurally irrelevant. What matters is the sequence, not the clock speed. In both cases: a bounded window of maximum narrative concentration → retail capital absorbs supply at peak valuation → insiders hold locked positions during the concentration window → insiders exit post-lockup → price reverts toward fundamental value. The mechanism is identical. The timescale is different because the asset class moves at different speeds, not because the psychology is different.

The low-float, high-fully-diluted-value listing crash — a pattern that has become routine in crypto markets — makes this structure explicit. A project lists a small percentage of its total token supply at a high implied valuation. Retail buyers pay the implied valuation. The team and early investors hold the majority of supply, locked. As lockups expire in stages, supply hits the market. The price reverts. The retail buyer paid the narrative peak price; the insider sold at or after the narrative peak. The project’s technology and roadmap are unchanged throughout. What moved was the information structure around the listing event, not the underlying asset.

The Information Structure of a Listing

Both the crypto token listing and the equity IPO produce a specific moment of maximum narrative concentration. This is not accidental. It is engineered.

The IPO process — roadshow, prospectus, institutional bookbuilding, retail allocation, listing day — is designed to concentrate attention, generate earned media coverage, and create a bounded window during which the narrative about the company reaches maximum intensity simultaneously with the first opportunity for public market participants to buy. The listing day is not chosen randomly. It is chosen to coincide with the moment when the largest possible number of buyers are paying attention and the largest possible volume of positive narrative is in the air.

Crypto listing mechanics replicated this structure and compressed it. The Telegram pump announcement is the roadshow compressed to a single message. The 18-second price peak is the listing day compressed to a window. The insider exit is the post-lockup selling compressed to minutes. Everything that takes months in an IPO takes minutes in a crypto pump because the underlying psychology — FOMO concentration followed by narrative dispersal followed by price reversion — operates at market speed in an asset class that never closes.

The critical insight that crypto markets arrived at through thousands of iterations, and that equity markets are now encountering in the context of SpaceX, is this: the listing event is not the beginning of the company’s public story. It is the climax of the private story. The maximum excitement, the maximum narrative, the maximum FOMO, all arrive precisely at the moment when buying is first possible. That is not a coincidence. That is the product.

Why SpaceX Is the Clearest Case

The SpaceX listing is uniquely useful as evidence for this argument because of the company’s genuine quality. SpaceX is not a fraud, a promotional vehicle, or a company with fabricated metrics. It is one of the most technically remarkable organisations in the history of aerospace. Falcon 9 has achieved the highest reliability rate of any orbital rocket ever flown. Starlink is a functioning global satellite internet network serving millions of customers. Starship is the most ambitious reusable launch vehicle ever built. By any operational measure, SpaceX is excellent.

This is what makes the valuation gap so analytically revealing. When a fraudulent company lists at an inflated price and the stock subsequently declines, the explanation for the decline is available: the fraud is exposed, the inflated metrics collapse, the real numbers surface. The price falls because the company wasn’t what it claimed to be.

SpaceX cannot use this explanation. The company is what it claims to be. The rockets work. The satellites are in orbit. The revenue is real. Morningstar’s $780 billion fair value does not dispute any of SpaceX’s operational achievements. Neither does Damodaran’s $1.3 trillion. Both analysts explicitly acknowledge the quality of the underlying business. Their models arrive at lower numbers because the relationship between SpaceX’s current financials and a $1.77 trillion market capitalisation requires a set of future assumptions — about Starlink’s eventual subscriber penetration, about Starship’s commercial launch cadence, about the pace at which net losses convert to free cash flow — that the listing price implicitly certifies as near-certain rather than possible.

When the stock declines from its IPO peak, the company will not have changed. The thing that changes is the narrative concentration. The listing window closes. The earned media cycle moves on. The retail FOMO disperses. What remains is the company, the financials, and the gap between the aspiration price and the price at which a patient long-term investor would be willing to buy.

Morningstar’s Advice Is the Tell

The most revealing sentence in any of the SpaceX IPO analysis is Morningstar’s advice to patient investors: wait for insider selling post-lockup.

Unpack what this means. Morningstar is telling investors that the right time to buy SpaceX is not on listing day — when the narrative is at maximum intensity and the price is at its peak aspiration level — but after the insiders who have been holding shares for years begin selling them into the market. After the lockup. After the first wave of informed sellers with long-dated information about the company begin accessing liquidity.

This is crypto patience in institutional language. The sophisticated participant in a crypto listing knows not to buy at the listing price. They know to wait until after the initial hype disperses, the early holders begin reducing positions, and the price reverts toward a level where the fundamental case can actually be made. The retail participant who bought on listing day absorbed the peak narrative concentration. The patient participant who waited for the lockup expiry buys at a price that reflects more equilibrium between supply and demand.

Morningstar published this advice in a mainstream financial research context and it was received as normal institutional guidance. The same advice in a crypto context would be labelled “waiting for the dump.” The underlying recommendation is identical. The language is different because the asset class and the audience are different. The mechanism is the same.

The Bridge: GameStop and the Infrastructure Migration

The pathway from crypto market psychology to equity market behaviour was not instantaneous. It required an infrastructure transition that happened in stages between 2019 and 2021.

The first stage was the commoditisation of retail trading. Commission-free trading via Robinhood eliminated the per-trade cost that had historically limited retail participation in rapid, sentiment-driven equity moves. The economics of buying and selling quickly in response to social media narratives changed from punitive to trivial.

The second stage was the migration of retail community infrastructure. Discord servers, Telegram channels, Reddit communities, and Twitter (now X) became the coordination layer for retail market sentiment in equities in the same way they had been for crypto. The same people. Often literally the same communities, now discussing both asset classes in the same channels. The tactics developed in crypto — coordinated buying on announcement, momentum amplification through social sharing, treating price movement as collective validation — arrived in equity markets because the community moved between them fluidly.

The third stage was GameStop, January 2021. The WallStreetBets short squeeze on GameStop produced the first moment where equity market participants, media, and regulators were forced to acknowledge that retail coordination could move a stock by hundreds of percent in days regardless of fundamentals. GameStop was a failing physical video game retailer. The quality of the company was irrelevant to the price action. What drove the stock was coordinated sentiment, short-squeeze mechanics, and the now-familiar sequence: announcement of the target → retail FOMO buying → price spike → eventual reversion.

GameStop established the pattern in equities. SpaceX completes its normalisation. The difference between GameStop and SpaceX is that GameStop was a struggling company on which the FOMO mechanic produced a price entirely disconnected from any plausible future value. SpaceX is an excellent company on which the FOMO mechanic has produced a price that Morningstar, Damodaran, and the former Nasdaq CEO all agree is substantially above any plausible near-term value. The mechanic is the same. The underlying company is different. The market psychology that drove the price is identical in structure.

What Comes After SpaceX

SpaceX is not an isolated event. It is the current clearest example of a pattern that will recur with every high-anticipation private company that eventually lists.

OpenAI’s private valuation has been reported at approximately $850 billion, set in funding rounds where institutional access was available to a limited set of participants and retail access was unavailable. When OpenAI eventually lists — if it lists — the same sequence will be present. Years of narrative accumulation. Maximum FOMO concentration at listing day. Institutional investors who participated in private rounds holding shares with a cost basis far below whatever the IPO prices at. Retail access beginning at the moment of maximum narrative intensity. Lock-up periods for early holders. Morningstar and Damodaran will publish their valuations. They will probably be below the listing price. The advice to patient investors will probably be the same: wait for the lockup.

The pipeline of private companies with large narrative premiums and eventual listing plans is well-populated. Stripe, Databricks, Anthropic, and others carry private valuations set in conditions that resemble crypto token prices more than they resemble public market valuations: small amounts of capital at large implied valuations, set by participants with information advantages over eventual public market buyers, in transactions that create the impression of a market-clearing price when they are actually bilateral agreements between sophisticated parties.

The convergence between crypto and equity market behaviour has been documented in price correlation data — Bitcoin trading at 92% correlation to the Nasdaq in late 2025. What the SpaceX IPO suggests is that the convergence is not just at the price level. It is at the structural level. The mechanics by which narratives are converted into prices, and by which prices subsequently revert, are operating by the same logic in both asset classes. The timescales are different. The vocabulary is different. The underlying dynamic is the same.

The Two Questions to Separate

Every discussion of the SpaceX IPO price collapses two questions that need to be kept separate. Keeping them separate is the discipline that crypto markets — at great retail cost, over many years — eventually enforced on their most attentive participants.

The first question: is SpaceX a great company? The answer is yes. The evidence for this is extensive and well-documented. Rockets land on drone ships. Satellites provide internet service to remote communities. Humans have returned to low Earth orbit. The engineering culture is genuinely exceptional by any aerospace standard. Anyone who says SpaceX is not a great company is wrong.

The second question: was $1.77 trillion the right price for SpaceX shares on June 12, 2026? This question has nothing to do with the first question. Morningstar’s $780 billion fair value is not a critique of SpaceX’s engineering. Damodaran’s $1.3 trillion is not scepticism about Starlink’s market potential. The former Nasdaq CEO’s comment about aspiration is not a dismissal of the company’s achievements.

Crypto markets developed the discipline of separating these questions slowly, and at great cost. The lesson was learned through thousands of token listings in which the project was technically legitimate — sometimes genuinely innovative — but the listing price had been set by the narrative concentration of the listing moment rather than by the fundamental value of what the tokens entitled their holders to. Many of those tokens subsequently declined in price. The teams building them continued building. The underlying technology continued developing. What changed was the narrative concentration, not the company. The price followed the narrative, not the company.

SpaceX is learning the same lesson at a different speed, in a different asset class, with better-dressed participants using more polished vocabulary. Morningstar does not say “DYOR.” Damodaran does not post to Telegram. But their message is structurally identical to what the most experienced crypto participants have been saying for years: separate the quality of the project from the rationality of the listing price. The two are not the same thing. They are not correlated. You can own a great company at a price that makes it a poor investment.

What the Pattern Tells Us

The SpaceX listing is, by market capitalisation, the largest IPO in US history. By narrative premium — the ratio of listing price to independent fair value estimates — it is also operating at the frontier of what the market has previously tolerated in the context of a profitable-trajectory, operationally credible company.

The fact that a Bloomberg columnist and CryptoRank both reached for the meme stock vocabulary within seven days of listing is not trivial. The vocabulary arrived fast because the pattern was recognisable fast. People who have watched crypto listings recognise the sequence. People who watched GameStop recognise the sequence. The retail participants who bought SPCX on June 12 at $135 are in the same information position as the retail participants who bought BVB at its 18-second peak: they bought the narrative at its maximum concentration. What they own is a security in an excellent company. What they paid was the aspiration price, not the equilibrium price.

This is the pattern that has now completed its migration from crypto markets into mainstream equities. It did not bring fraud with it. It brought psychology. The coordination, the FOMO, the gap between narrative price and fundamental value, the lock-up as the structural tell, and the eventual reversion — all of it arrived without a single actor intending to run a pump-and-dump. The infrastructure of modern retail markets — instant access, social media amplification, zero-commission trading, a culture that treats price movement as collective validation — does the work automatically. No Telegram channel required.

SpaceX will continue to build rockets. The Falcon 9 will continue to land. Starship will continue its development. None of that is in question. The question that Morningstar, Damodaran, and the former Nasdaq CEO have each answered in their own way is the only question that matters for investors: what did you pay, and is the price rational relative to any defensible valuation of what you own?

Crypto markets learned this distinction the hard way, across a decade of listing events that peaked in seconds and reverted in minutes. Traditional equity markets are learning it now, in the context of the most credible company imaginable, across days and weeks rather than seconds and minutes. The timescale is different. The lesson is the same.

The Narrative of the SpaceX IPO: How FOMO Is Constructed, and Why It Works Until It Doesn’t

Holiday’s framework for understanding media and narrative draws on the Stoic tradition, which distinguishes between things that are in our control and things that are not. Applied to investment markets, the useful insight is that the FOMO narratives that drive retail behaviour in pre-IPO markets are not spontaneous eruptions of collective enthusiasm — they are constructed, amplified, and sustained by specific actors with specific interests, and they follow predictable patterns. The SpaceX IPO narrative is one of the most deliberately constructed in recent market history.

The construction began not with the IPO announcement itself, but with the secondary market for SPCX shares and the sustained media coverage of SpaceX’s mission and Elon Musk’s reputation for transformative technology. The FOMO mechanics require three elements: a compelling story that connects the asset to a transformative future, perceived scarcity (access is limited, you might not be able to participate), and social proof (other credible investors are getting in). All three were systematically cultivated in the SpaceX pre-IPO narrative: the mission to Mars and satellite internet domination provided the transformative story; the SPCX lockup and 4% float mechanics created literal scarcity through a 4% float that ensured most investors simply could not participate on the public market; and the participation of institutional names in secondary SpaceX shares provided the social proof that the narrative was credible.

The Stoic question is: what is in the investor’s control here? The answer is the evaluation framework — whether the investor assesses SpaceX’s actual business fundamentals (Starlink subscription revenue, launch economics, capital requirements) or accepts the narrative construction at face value. The FOMO narrative is designed precisely to make the fundamental evaluation seem irrelevant. You don’t ask what Twitter’s revenue model was in 2010 if you’re being told that social media is changing how humans communicate. You don’t ask what SpaceX’s EBITDA multiple justifies if you’re being told that SpaceX is changing how humans access the internet and eventually how they become multi-planetary. The narrative does not require fundamental justification; it requires sufficient social proof to maintain belief.

Holiday’s analysis of how narratives eventually break focuses on the gap between the story and the material reality. Narratives break when the material evidence they predicted fails to materialise at the scale or pace the story required, or when a counter-narrative with sufficient credibility emerges to disrupt the consensus. OpenAI’s $1 trillion IPO and the FOMO contagion pattern shows the adjacent case: OpenAI’s $1 trillion IPO valuation is the most extreme contemporary example of a narrative-led valuation where the fundamental evidence — revenue at scale, path to profitability, competitive moat against open-source alternatives — is secondary to the story that OpenAI is building something civilisationally transformative. SpaceX and OpenAI share the same narrative template: transformative leader, audacious mission, conventional financial metrics that look absurd at the claimed valuation but seem beside the point given the stakes.

the end of the easy-technology era driving narrative-led investing is the macro context that makes these narratives particularly powerful in 2026: when conventional asset classes are being disrupted and the standard mental models for valuing companies are being challenged by AI and automation, the psychological appeal of a company that is clearly doing something new is very high. The real-world asset tokenisation and pre-IPO market access creates an additional FOMO channel: if private equity tokenisation allows broader access to pre-IPO SpaceX shares through blockchain-based instruments, the scarcity argument is simultaneously maintained (it’s still hard to get in) while the social proof expands (crypto-native investors are now also participating). This is a sophisticated narrative amplification mechanism.

The Stoic discipline the FOMO narrative most actively undermines is the attribution illusion in pre-IPO market analysis: the ability to accurately assess causation between what you believed and what actually happened. FOMO investors in pre-IPO narratives rarely build rigorous attribution models for their returns. When SpaceX shares appreciate, the attribution is the original thesis — the mission is real, the technology is transformative. When they depreciate, the attribution is temporary market noise or unfair regulatory treatment. The narrative framework is self-sealing against falsification. Holiday’s counsel is not to avoid these investments — it is to be aware that the narrative is a construction, to identify the specific falsifiable predictions embedded in the thesis, and to decide in advance what evidence would cause you to update. The FOMO narrative works until it doesn’t, and the investors who survive the break are the ones who decided before they invested what would break it.