Kevin Warsh chaired his first Federal Open Market Committee meeting on June 16–17, 2026. Rates were held. The dot plot was revised to show zero rate cuts for 2026 — down from one cut projected in May. Fed funds futures now price a 66% probability of a rate hike before year-end. Inflation is at 3.8%. Bitcoin is trading at approximately $65,000, roughly 50% below its all-time high. The macro environment that Bitcoin’s foundational investment argument was constructed to test has now arrived in measurable, central-bank-confirmed form. The test has been running for six months. The results are not encouraging for the thesis.

What Warsh Represents

The June 17 rate decision is not the story. Warsh holding at 98.6% probability was the most priced-in outcome of the year. What matters is what his appointment, his first meeting, and the revised dot plot collectively signal about the forward monetary environment.

Warsh opposed the Fed’s post-2008 quantitative easing programs publicly and in real time — on the record, while serving as a Fed governor, arguing that balance sheet expansion was inflationary and that the exit would be disorderly. He has spent the intervening years arguing for a more aggressive posture toward inflation: not Volcker-style shock therapy, but a willingness to stay restrictive longer than the market expects and to treat above-target inflation as a structural problem rather than a transitory inconvenience.

His June 17 press conference delivered exactly what his appointment implied. The dot plot revision from one cut to zero cuts for 2026 is not a large numerical change. In context, it is a signal: Warsh does not believe the disinflation path is sufficiently advanced to project relief. His characterisation of 3.8% CPI as a persistent rather than temporary problem — requiring a sustained restrictive response — is the characterisation of a chair who is not looking for an exit.

The market’s 66% hike probability by year-end is the aggregate judgment of institutional participants who have now incorporated Warsh’s posture, the inflation data, and the revised dot plot. Two in three dollars of bet says the next rate move is up, not down.

The forward environment this produces is specific: elevated inflation, above-neutral policy rates, no rate relief projected, and a non-trivial probability that rates rise further before any relief arrives. This is a prolonged high-rate, high-inflation environment in which monetary policy is actively tightening against a fiscal backdrop that is expanding. It is, by the precise terms of the Bitcoin investment thesis, the environment Bitcoin was built for.

The Thesis, Stated Precisely

The Bitcoin inflation hedge argument has been stated in many forms over fifteen years. It is worth reconstructing it precisely rather than arguing against a straw version.

The core claim is structural: Bitcoin is a hedge against fiat currency debasement. It is not primarily a bet on short-term price appreciation. It is a claim that in environments where central banks expand money supply, allow inflation to persist above target, or permit fiscal deficits to compound in ways that undermine confidence in sovereign debt, the fixed-supply scarcity of Bitcoin — 21 million coins, fully predictable issuance, no central authority with the power to change those parameters — should cause capital to flow toward it as a store of value relative to debasing fiat currencies.

The specific environments the thesis predicted Bitcoin would perform in are not vague. They are precise: inflation above central bank targets. Fiscal expansion that compounds sovereign obligations. A central bank unable to restore price stability without inducing severe economic damage. Dollar weakness from deteriorating fiscal credibility. A political environment in which the will to maintain fiscal discipline is insufficient to arrest deficit growth.

Check each against 2026: CPI at 3.8% against a 2% Fed target. The Big Beautiful Bill adding an estimated $3–5 trillion to the US deficit over ten years, passed and signed. Warsh inheriting an inflation problem his predecessor left unsolved, with hike odds at 66% rather than the rate relief the market expected. The dollar index under pressure from yield dynamics and the first US credit downgrade from Moody’s. A political environment in which the fiscal expansion was legislated by choice, not imposed by crisis.

Every condition the thesis specified is present. The hedge test has been running since January, in conditions that match the thesis’s own definition of the environment it was designed for.

What Bitcoin Did

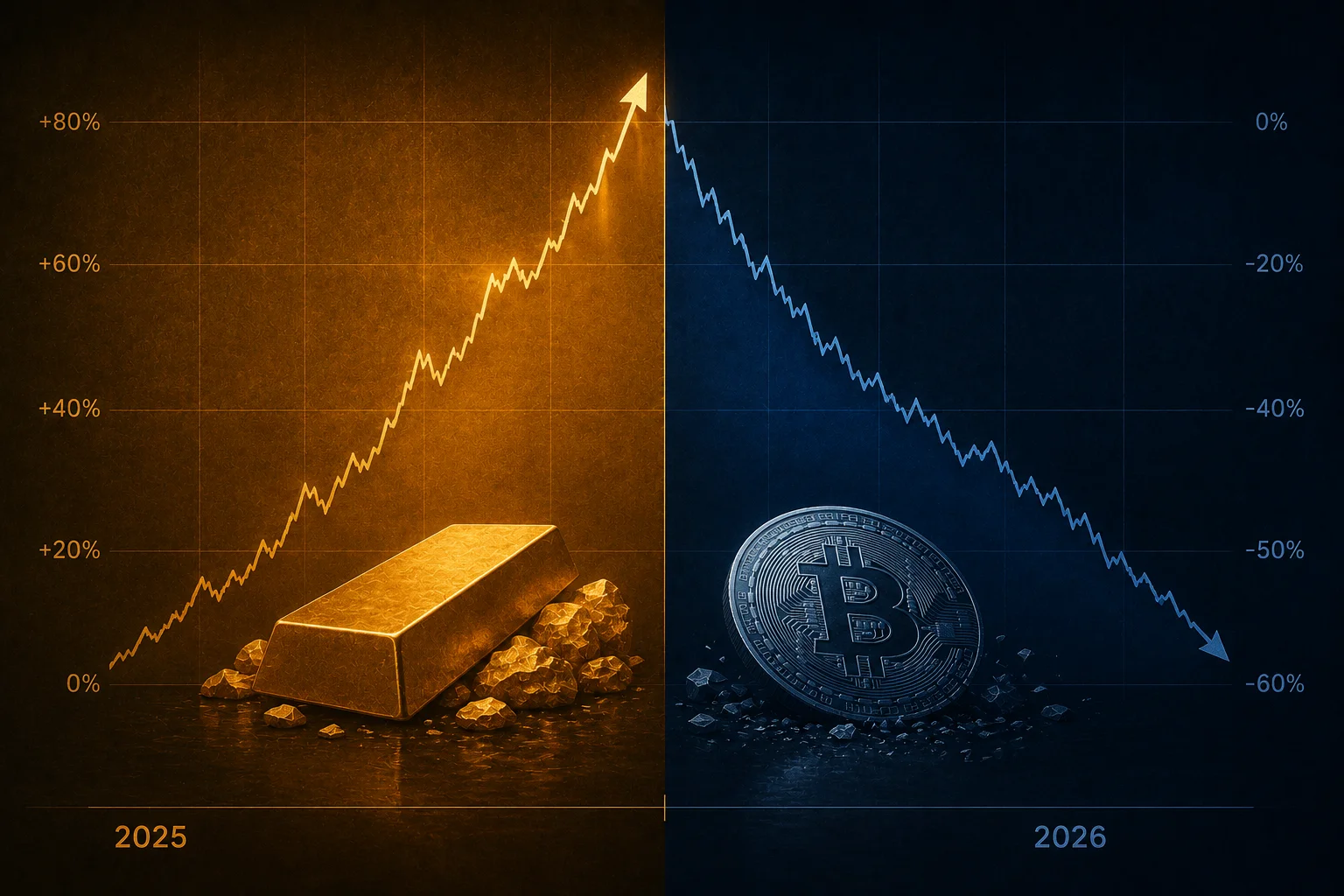

Bitcoin began 2026 approaching its all-time high. By mid-June, it is down approximately 50% from that peak. Gold, over the same period and in the same macro environment, is up approximately 80% from its early 2025 levels.

The six-month correlation between Bitcoin and gold was measured at -0.88 in late 2025 data. They are moving in nearly perfect opposition. One is rising in the macro environment the Bitcoin thesis predicted would be favourable. The other is falling in the same environment. The question of which is which is the subject of six months of empirical data.

The institutional infrastructure built to channel adoption has also behaved in a specific way. BlackRock’s IBIT ETF saw a 12-session consecutive outflow streak in early 2026 — the sustained institutional infrastructure that was supposed to represent Bitcoin’s maturation as an asset class generating sustained net outflows during the period of peak macro justification for the thesis. Strategy reported a $12.27 billion paper loss in a single quarter on its Bitcoin holdings. Michael Saylor, the most prominent institutional advocate for Bitcoin as a balance sheet asset, sold 32 BTC in May — the first sale from the man whose brand was built on “never sell.”

None of this is a temporary dislocation. It is a sustained pattern covering the full period during which the macro conditions the thesis required have been confirmed. Saylor’s own rationalisation sequence — five separate explanations across three months — documents the distance between what the thesis predicted and what the data produced.

The Mechanism: Three Reasons the Hedge Does Not Activate

The gap between a theoretically sound inflation hedge argument and an empirically non-functional inflation hedge requires explanation. There are three mechanisms.

The Classification Problem

Institutions do not classify Bitcoin as a hedge asset. They classify it as a risk asset. In portfolio construction, Bitcoin sits in the same risk bucket as growth equities, high-beta technology stocks, and speculative positions. When risk appetite contracts — which it does when the Fed signals or enacts tighter monetary conditions — everything in the risk bucket falls together, regardless of its theoretical supply characteristics.

Bitcoin’s six-month correlation to the Nasdaq has been measured at approximately 92%. That figure is not a diversifier property. It is a technology sector exposure with higher volatility. For the inflation hedge to activate, Bitcoin must decouple from risk assets during inflationary stress and demonstrate the haven flow dynamics that would justify reclassifying it in institutional portfolios. So far in 2026, that decoupling is not occurring.

The classification problem is circular in a way that traps the thesis: Bitcoin will be reclassified as a hedge asset when it demonstrably behaves as one. It will demonstrably behave as one when institutional portfolio models reclassify it and allocate to it on that basis. In the meantime, it behaves as a risk asset because that is how institutional models currently treat it, and therefore continues to not qualify for reclassification. The 2026 data is one more data point extending the wait.

The Carry Cost Differential

Bitcoin pays no yield. Gold pays no yield. In a high-rate environment — Fed funds above 4%, T-bills yielding above 4% — holding either asset carries an explicit opportunity cost. The question is how that opportunity cost is priced against the hedge value of the asset.

Gold has a multi-century track record as a monetary crisis asset, sovereign wealth component, and central bank reserve instrument. The opportunity cost of holding gold is priced against deep institutional conviction, embedded in regulatory frameworks and sovereign mandates, that gold preserves value across monetary stress events. That conviction does not need to be re-earned in each cycle. It is structural.

Bitcoin’s hedge track record is approximately fifteen years long, with no prior test in a sustained, central-bank-confirmed inflation environment where the alternative is a 4%+ risk-free rate. The opportunity cost of holding Bitcoin is being priced against a hypothesis — one that is theoretically coherent, has institutional advocates, and has performed well in zero-rate environments — but that has not yet been empirically confirmed in the specific macro regime it was designed to address. In a high-rate environment, the unconfirmed hypothesis does not win the carry comparison against the established reserve asset.

The Inflation-Tightening Loop

The Bitcoin thesis operates at the level of monetary theory: inflation erodes fiat purchasing power; a fixed-supply asset should appreciate relative to depreciating fiat. This logic is sound at the monetary level.

It is incomplete at the financial market level, because it omits the central bank’s response function.

Inflation above 2% in a central bank regime with a 2% mandate does not produce a static environment in which Bitcoin can quietly appreciate against a debasing dollar. It produces a central bank response: rate hikes, balance sheet contraction, tighter financial conditions. That response contracts equity multiples, pressures risk assets, and reduces the appetite for speculative positions. Bitcoin, classified as a risk asset and correlated at 92% to the Nasdaq, falls with the risk complex.

The trap is structural: Bitcoin needs the inflation environment to validate its hedge thesis. But the inflation environment triggers the Fed response that hurts Bitcoin as a risk asset. The inflation it was designed to benefit from creates the monetary tightening that punishes the asset class it is actually classified in. The conditions for the thesis to be confirmed are the conditions that prevent its confirmation.

Warsh’s June 17 meeting extended this loop. By erasing 2026 rate cuts from the dot plot and leaving hike odds at 66%, he confirmed that tighter conditions are the forward path. Bitcoin faces higher rates, continued risk-off pressure, and no macro pivot to relieve the tightening cycle. The inflation that should be its best argument is producing the policy response that hurts it most.

Why Gold Is Not Having the Same Problem

Gold’s 80% rise in the same environment that produced Bitcoin’s 50% decline requires explanation, because the classical analysis of gold and interest rates would not predict gold outperforming during a rate-rise cycle.

Higher real rates are, in the textbook account, a headwind for gold. Gold pays no yield, so as real rates rise, the opportunity cost of holding gold increases, and capital should flow toward interest-bearing alternatives. By this logic, Warsh’s hawkish posture should be bad for gold as well as Bitcoin.

The data says it isn’t. Gold has risen through the Warsh appointment, through the dot plot revisions, and through the inflation readings that have kept rates elevated. The reason is that gold is not primarily trading as an interest rate instrument in 2026. It is trading as a sovereign credit instrument.

Central banks — particularly those outside the dollar reserve system, but increasingly within it — are accumulating gold as a hedge against US fiscal credibility. The fiscal expansion — the Big Beautiful Bill, the Moody’s downgrade, the debt-to-GDP trajectory — has introduced a long-duration risk to holding dollar-denominated assets. Gold’s response to that risk is distinct from its response to a rate cycle: the fiscal credibility mechanism overrides the real-rate mechanism in 2026 because the magnitude of the fiscal deterioration is larger than the magnitude of the rate headwind.

Bitcoin’s theoretical claim to the same trade is direct: it is a non-sovereign, fixed-supply asset that should benefit from deteriorating confidence in sovereign credit. The claim is structurally identical to the gold-as-sovereign-hedge argument. Gold is demonstrating empirically that this argument has force — that institutional capital will move toward non-sovereign assets in response to fiscal credibility deterioration.

Bitcoin is demonstrating that the argument, while theoretically valid, is not being acted on in Bitcoin’s case. The institutional mandate that covers gold does not yet cover Bitcoin. The sovereign wealth, central bank, and long-duration institutional allocation that is driving gold’s performance is not available to Bitcoin at the same scale, regardless of the shared theoretical basis.

The -0.88 correlation between Bitcoin and gold over six months is not evidence that they are different kinds of assets. It is evidence that the same underlying macro thesis is being expressed in two assets with very different institutional access. Gold captures the institutional trade. Bitcoin does not.

The Prior Test Claims

It is worth accounting for the previous moments when Bitcoin advocates declared the hedge thesis proven, because 2026 is not the first environment claimed as the confirming test.

The 2020–2021 period was the first candidate. Bitcoin rose dramatically during the period of maximum Fed balance sheet expansion and near-zero interest rates. The thesis absorbed this as confirmation: monetary expansion drives Bitcoin appreciation. The problem with this reading is that 2020–2021 was simultaneously the peak of pandemic risk-on sentiment, the period of maximum retail speculative appetite, and the era of zero-rate-driven asset inflation across equities, real estate, and collectibles. Bitcoin rising during the everything rally does not isolate the inflation hedge mechanism from the speculative momentum mechanism.

The 2022–2023 period was the second test. Bitcoin fell dramatically as the Fed raised rates from zero to 5.25%. The thesis absorbed this as a liquidity crisis specific to crypto: FTX’s collapse, Three Arrows Capital, the contagion through the crypto lending complex. The argument was that the failure was idiosyncratic to the crypto sector, not a test of the inflation hedge claim per se.

The 2026 environment is cleaner. There is no FTX equivalent — no crypto-sector-specific collapse to absorb the decline as idiosyncratic. There is no pandemic-era speculative mania to absorb the prior rise as something other than hedge mechanics. What there is: a sustained, central-bank-confirmed inflation environment, a hawkish Fed chair, fiscal expansion, and Bitcoin down 50% while gold is up 80%.

The test that the thesis demanded — the one where inflation arrives in sustained, confirmed, above-target form, with a central bank that hasn’t resolved it and a fiscal backdrop that won’t help — is the test 2026 is running. And the test is, six months in, not producing confirmation.

What Warsh’s Meeting Adds to the Record

The June 17 FOMC meeting does not change the underlying empirical record. It extends the duration of the conditions under which the record is accumulating.

Before June 17, a Bitcoin advocate could argue that the environment was temporary — that rate cuts were coming, that the dot plot showed relief in the second half of 2026, that the tightening cycle was near its end. After June 17, that argument requires a material revision. Warsh has not projected relief. He has projected persistence. The dot plot that showed one cut for late 2026 in May now shows zero cuts for 2026 in June. The 66% hike probability means the most likely next move is a rate increase, not a reduction.

This matters for the thesis because the Bitcoin inflation hedge argument has always carried an implicit timeline assumption: eventually the conditions will be so undeniable, so extended, and so broadly acknowledged that institutional capital will have no choice but to treat Bitcoin as the hedge it claims to be. Each FOMC meeting that extends the conditions without producing the reclassification extends the period over which the thesis has failed to activate.

The counter-argument is available: this is still early. Bitcoin adoption is incomplete. The institutional reclassification is a slow-moving process. The thesis will be confirmed when Bitcoin’s market depth, regulatory clarity, and institutional infrastructure have matured sufficiently to support the haven-flow mechanics. The 2026 data is a data point, not a verdict.

This counter-argument may be correct. But it is not the counter-argument that Bitcoin advocates were making when they described 2026’s macro conditions as the eventual proof of concept. The argument that the test hasn’t run yet — when 3.8% inflation, a hawkish Fed chair, 66% hike odds, Big Beautiful Bill fiscal expansion, and a Moody’s downgrade are all simultaneously present — requires explaining what additional macro confirmation the thesis needs before the test is considered valid. The environment that was supposed to be the proof is here. Something else must account for the gap between the theory and the price.

What Remains

Bitcoin may recover. Assets reprice. Markets cycle. The 50% decline from the all-time high is not permanent, and the performance gap relative to gold may narrow. None of that is analytically excluded by the 2026 data.

What the 2026 data does constrain is the forward claim that Bitcoin’s inflation hedge thesis is waiting for its moment of confirmation. If the moment is not 3.8% inflation, zero projected cuts, 66% hike odds, fiscal expansion legislated into law, and a Moody’s AAA downgrade — then what is the moment? When advocates specify the conditions, those conditions are present. When the conditions are present, a different explanation emerges for why this particular environment isn’t the real test.

Warsh’s first meeting produced a clear forward path: persistent inflation, no rate relief, rising hike probability. The macro environment that Bitcoin’s thesis identified as its best-case scenario is being confirmed as durable. Bitcoin is down 50% from its all-time high. Gold is up 80%. The -0.88 correlation is a measurement, not an editorial judgment.

The inflation hedge that was built for this moment has not performed in this moment. The June 17 FOMC meeting extended the conditions under which that sentence remains true. It will keep extending them until Warsh pivots, until Bitcoin decouples from the risk complex, or until the thesis is revised to specify a different kind of environment as the real test.

None of those three things happened on June 17.

The Decision Science of the Bitcoin Inflation Hedge: What the Evidence Actually Supports

The framing problem with the Bitcoin inflation hedge thesis is not that it’s wrong — it’s that the question being asked is too vague to be wrong or right. ‘Does Bitcoin hedge inflation?’ is not a decision-relevant question. The decision-relevant question is: under what specific conditions does Bitcoin deliver positive real returns during inflationary periods, what is the probability of those conditions holding, and what is the expected value of holding Bitcoin as an inflation hedge across all the scenarios where inflation matters to a portfolio?

Annie Duke’s framework for good decision-making starts with separating the quality of the decision from the quality of the outcome. The fact that Bitcoin rose during the 2021–2022 inflation surge is not strong evidence that it is an inflation hedge, because the same period included massive monetary expansion, risk-asset FOMO, and retail crypto adoption — any of which could have driven the price regardless of inflation dynamics. And why Bitcoin’s rate correlation broke in 2026 from 2026 demonstrates the flip side: Bitcoin held $90,000+ while the Fed held rates elevated, but the mechanism was not inflation hedging — it was institutional ETF demand and corporate treasury mandates creating inelastic buyers.

The decision-science approach to evaluating this thesis requires isolating the mechanism. An inflation hedge works because the asset’s value is inversely correlated with the purchasing power decline that inflation represents. Gold is the canonical example: its hedge value comes from its role as a monetary store that is not subject to debasement. The gold thesis has survived multiple inflationary cycles because the mechanism — scarcity, cross-cultural monetary recognition, central bank accumulation — is stable and well-documented. gold’s safe-haven thesis in 2026 in 2026 reflects the continuation of that mechanism: central banks are buying gold precisely because they understand that it is a claim on real assets that is not contingent on any government’s fiscal discipline.

Bitcoin’s claim to the same status is structurally weaker because the mechanism depends on conditions that may not hold in a severe inflation scenario. The inflation hedge thesis requires: (1) that market participants maintain Bitcoin’s value as a monetary store during the same conditions that cause inflation, which means not selling Bitcoin to fund the nominal expenses that inflation makes more expensive; (2) that the regulatory environment doesn’t restrict Bitcoin access precisely when it’s most needed as a hedge (governments historically restrict capital flight during inflationary crises); (3) that the correlation between Bitcoin and risk assets doesn’t dominate the inflation-hedge signal during a crisis. Treasury auction dynamics and bid-cover ratios indicate that the rate-sensitive fiscal environment creates correlation risk that the simple inflation hedge narrative ignores.

The expected value calculation across realistic inflation scenarios is unfavourable for using Bitcoin as a primary inflation hedge. In mild inflation scenarios (2–4%), Bitcoin probably holds value but so do equities and TIPS — the hedge is redundant. In moderate inflation scenarios (4–7%), the Fed typically responds with rate hikes, which historically correlated negatively with Bitcoin prices (the 2022 case). In severe inflation scenarios (7%+), government intervention risk is highest and correlation with distressed risk assets is highest. the structural end of the easy-technology era identifies the structural conditions — the end of zero-rate policy and easy-money tech investment — that created the 2022 inflation and Bitcoin’s simultaneous collapse. The scenarios where Bitcoin is most needed as an inflation hedge are the scenarios where it is most likely to underperform.

The ECB-Fed policy divergence creates an additional variable: if the ECB is cutting rates while the Fed holds, the inflation dynamics in EUR-denominated portfolios differ from USD-denominated portfolios in ways that change the expected value of Bitcoin as a hedge in each jurisdiction. A European investor holding Bitcoin as an inflation hedge faces a different scenario distribution than a US investor — the EUR weakness from ECB cuts creates its own inflation pass-through, and Bitcoin’s USD-denominated pricing means EUR inflation doesn’t directly translate to Bitcoin hedge performance. These are the kinds of second-order probabilities that the simple ‘Bitcoin hedges inflation’ framing erases. The correct approach is to model the hedge properties explicitly, assign probabilities to each scenario, and size the position according to the expected value — not to adopt a binary hedge-or-no-hedge framing based on a single historical episode.